Just 18 months ago, Moderna Inc. was an early-stage biotechnology company working on a new way of making vaccines worth $6.5 billion. Today, after it developed and delivered one of the fastest-arriving and most effective shots against Covid-19, Moderna’s market value is approaching $100 billion.

Some of the stock's 1,000% gain is undoubtedly warranted. Wall Street analysts expect Moderna's vaccine, which uses new messenger-RNA technology, to net a historic $17.6 billion in revenue this year. But the company's valuation is now in the same league as drugmakers that, unlike Moderna with its one vaccine, have multiple marketed medicines. Holding the stock at this level requires some particular assumptions about the future of the pandemic and a heroic tolerance for concentration of risk.

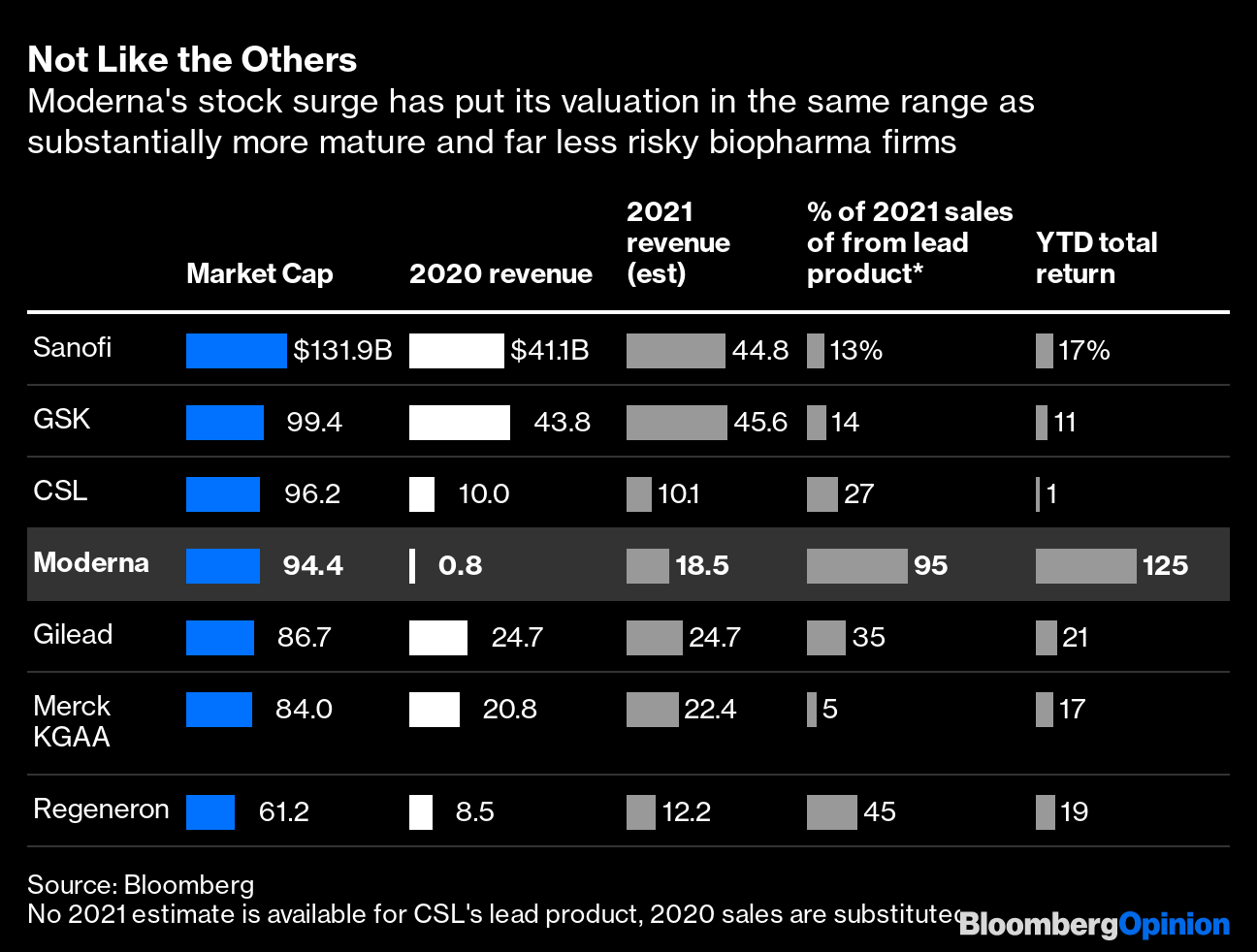

Not Like the Others

Moderna's stock surge has put its valuation in the same range as substantially more mature and far less risky biopharma firms

Source: Bloomberg

No 2021 estimate is available for CSL's lead product, 2020 sales are substituted

The central question for Moderna investors is how long Covid vaccine sales will last. The market for first and second doses is shrinking each day and is starting to concentrate around developing nations where prices are lower. As a result, the company's prospects rely heavily on booster shots aimed at providing extra protection should immunity from the initial round of vaccinations fade, as many expect. While mRNA vaccines will likely be the boosters of choice because of their effectiveness and safety, it's unclear how many people will get a Moderna top-up (Pfizer Inc. and BioNTech also make a highly effective mRNA vaccine). That helps explain why Wall Street estimates for Moderna’s 2021 sales range a bit widely, from $13 billion — which would represent a decline from this year’s consensus forecast — to $22.2 billion, according to data compiled by Bloomberg.

One can certainly make a case for the higher range. Countries that use AstraZeneca PLC’s vaccine or others that offer less protection may offer boosters just to be safe. The potentially dangerous combination of waning vaccine immunity and variant spread could lead to even broader uptake. Booster demand will be concentrated in wealthier nations, letting Moderna charge more and compensate for declining volume. And there would be additional upside if variant-specific shots are required because Moderna's adaptable technology and established manufacturing should give it an advantage in rolling out second-generation vaccines.

But at least for now, two mRNA doses appear to hold up against bad outcomes from the highly infectious delta variant first identified in India. So does Johnson & Johnson’s one-shot vaccine, according to recently released data. Delta is driving a wave of infections in the heavily vaccinated U.K., but relatively few hospitalizations so far, even with significant use of AstraZeneca’s shot. In addition, a recently published study suggests that mRNA vaccines generate a broad immune response that may last for years. So boosters could very well be delayed or limited to people who have weaker immune systems. A longer interval will allow potential competitors such as Novavax Inc., Sanofi and GlaxoSmithKline PLC to catch up. Given all this, the lower revenue scenario is a distinct possibility.

Even if Moderna's Covid vaccine sales don’t peak until next year, a decline is inevitable, and it could be steep. The company’s lack of other revenue sources will magnify the reaction to any Covid disappointment. Expectations for its drug pipeline are justifiably high after the success of its vaccine, but you can only hang so much of a $95 billion valuation on distant and unproven products. Moderna's most advanced non-Covid project, a cytomegalovirus vaccine (to protect against a virus that's harmless to most but can cause birth defects if passed from a mother to her unborn child), will only begin a final-stage trial this year.

Recent pharma history shows what can happen to rich valuations when a golden goose runs out of eggs. Here, Gilead Sciences Inc. offers an instructive example. The company launched a groundbreaking hepatitis C drug in late 2013. Sales spiked to an astonishing $19.1 billion in 2015 but then plunged as competitors arrived. Gilead's value followed suit, dropping as much as $100 billion from its peak of almost $180 billion. Of course, the comparison isn't perfect. Gilead had a reliably growing multibillion-dollar HIV drug franchise to provide a floor.

Roller Coaster

It turns out that shareholders don't like it when companies make a lot of money and then start making less money

Source: Bloomberg

In Moderna’s case, a key unknown is how well mRNA technology will work to prevent other diseases. The technology's adaptability may be most beneficial in an epidemic or against viruses like influenza that change frequently, and that's not generally a valuable niche. The company hopes to use mRNA to treat cancer and rare disease, but those early efforts are particularly uncertain. Either way, while Moderna will retain a first-mover advantage in mRNA and unique expertise, the field will get more crowded as other drugmakers invest heavily in the technology.

I've been wrong about Moderna's valuation before, calling it rich after its IPO in 2018. But even in the rosiest of scenarios, it seems stretched now. And this time, if there is a reckoning, it has a lot further to fall.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

To contact the editor responsible for this story:

Beth Williams at bewilliams@bloomberg.net

"really" - Google News

July 06, 2021 at 05:00PM

https://ift.tt/3hBEtf2

Is Moderna's Vaccine Breakthrough Really Worth $100 Billion Market Value? - Bloomberg

"really" - Google News

https://ift.tt/3b3YJ3H

https://ift.tt/35qAk7d

Bagikan Berita Ini

0 Response to "Is Moderna's Vaccine Breakthrough Really Worth $100 Billion Market Value? - Bloomberg"

Post a Comment